Sample The New Eugenics Research Paper. Browse other research paper examples and check the list of research paper topics for more inspiration. If you need a religion research paper written according to all the academic standards, you can always turn to our experienced writers for help. This is how your paper can get an A! Feel free to contact our research paper writing service for professional assistance. We offer high-quality assignments for reasonable rates.

1. Introduction

With the continued progress of the Human Genome Mapping Project to identify all the genes in the body and the technologies that are developing from it, there is renewed concern about eugenic applications. Eugenics means using science for the qualitative and quantitative improvement of our genetic constitution. The subject was initiated by the Ancient Greeks and developed enthusiastically by a Victorian scientist, Francis Galton, with considerable support from his cousin Charles Darwin in the latter half of the nineteenth century (Kevles 1995). Its scope has increased enormously since the recent revolution in molecular genetics. Genetic databases can be easily obtained for individuals either before or at birth, and are being constructed for entire populations; and genetic markers are being developed to predict risks of developing cancer, diabetes, early heart attacks, and dementias. These markers can be used for diagnosis to see if the early embryo possesses deleterious alleles predisposing to disease or even carries personality ‘traits’ such as a tendency to become alcoholic, obese, or neurotic in later life. Such embryos can be discarded without the need to terminate pregnancy in favor of ones with ‘better’ genetic endowments leading to the concept of ‘designer babies.’ Genetic markers can also be used in childhood to predict the likelihood of developing common diseases in later adult life and this may lead to discrimination by insurance industries, employers, adoption agencies, and other state institutions.

Academic Writing, Editing, Proofreading, And Problem Solving Services

Get 10% OFF with 24START discount code

The past history of eugenics has been appalling, with gross abuses in Germany between 1933 and 1945 when sterilization and mass extermination were performed. Revulsion generated by the laws of any state that interferes with people’s reproductive choices or freedoms—whether for the theoretical purpose of improving the ‘gene pool’ or for other reasons such as the current demographic policy of China to restrict one child per family leading to changes in the gender ratio—has led to eugenics acquiring an evil reputation (Duster 1990).

However, the new genetic technologies are here to stay. To prevent such abuses for the future there have to be mechanisms to regulate these new techniques when applied to medical and social problems.

2. The Need For Regulation

The new eugenics requires regulating the varied and powerful social applications that are being developed, for example, ‘designer’ childbirth, cloning, disease prediction, insurance, industry, etc. Society will expect rules and laws to protect them from the excesses of overenthusiastic doctors and scientists, and from the greed and ambition of global corporations (Rifkin 1999).

Society’s response to the new developments is not going to be easy. There is a variable and fine line that demarcates law from ethics. The line separates what can be left to individuals to choose for themselves from what requires enforcement by the law. The law and rules of professional bodies related to eugenics at present are a mass of inconsistencies. One problem is that major public interests such as education, health, and welfare, which should be the proper concern of law, are so intertwined with the realm of private and individual interests of the family. The latter could be left to individuals to work out for themselves based on their own wishes, needs, and preferences. For the future we will have to balance the practical applications arising from the new research against the need to protect both individuals and society from its dangers; and to resolve in some way the many conflicts of values that will arise.

Law is needed to negotiate between fact and value, and should be firmly based on reason and judgment (Brownsword et al. 1998). But unfortunately the facts and techniques are changing all the time from month to month. One regulatory body, the UK Human Fertilisation and Embryology Authority, developed a set of rules to cover the use of human embryos produced by test-tube fertilization. But these rules do not specifically apply to embryos produced by nuclear transfer techniques. As of 1999 there is at present no UK legislation in force specifically directed at human cloning. When human cloning was banned in the USA, laboratories there started to use enucleated egg cells from the cow for transfer of a human nucleus to make cow–human hybrids. So the law may have to be changed again; and just as quickly the scientists will find a way round it.

The problem is likely to get worse as the demand for new treatments of fertility is constantly increasing. This is partly because there is a continuing fall in the number of babies available for adoption and a growing tendency for women to delay motherhood to establish their careers first until they reach an age when complications of childbirth are more likely to arise. For example, the number of women undergoing in vitro fertilization rose from approximately 12,000 in 1992 to 19,000 in 1994 in Western countries.

3. Regulatory Agencies

Legislators do not always understand the intricacies of the science they are called upon to regulate. So sets of regulatory agencies composed of a small group of scientists, lay-people, and lawyers are set up to provide recommendations and guidelines. These regulatory bodies have proliferated and range from local hospital ethical committees to national ethical committees to international bodies such as the UK Human Genetics Advisory Commission, the Advisory Committee on Genetic Modification, the UK Human Fertilisation and Embryology Authority, and the European Medicines Evaluation Agency. It is not surprising that with the numbers involved they are already starting to give confused or contradictory advice. To give one example: the UK Alzheimer’s Disease Genetics Consortium have drawn up guidelines for what they consider to be the best possible practice for the genetic diagnosis of Alzheimer’s dementia. They propose that before genetic testing informed consent should be obtained from the patient but the results should not usually be given back to the patient, except under the most exceptional circumstances, and then only after the appropriate counseling. However, another body, the Association of British Insurers, have demanded as a part of their genetic policy that for the purchase of insurance products of greater than £100,000 the results of genetic tests should be declared to them. A third body, the UK Human Genetics Advisory Commission, recommended a moratorium for two years on the use of genetic information for insurance purposes until one can find out what actuarial relevance it may have. But this was not adopted—it was considered by Government that the insurance industry should manage its own affairs without the need for interference (Galton and Ferns 1999).

Additional problems of leaving ethical decisions involving the genetic technology to locally interested consortia is that wider issues may be overlooked. For example, apo-E genotyping has been in use as an important diagnostic aid for blood fat disorders in hospital clinics worldwide for the past decades. This information, now available in casenotes and medical reports, can be used to predict the occurrence or diagnosis of Alzheimer’s dementia in some of the patients who were tested (Galton and Krone 1991). There is no clear policy for confidentiality of these records or how they should be used. Who should have access to the information? The individuals were initially tested for a different condition, namely a cholesterol transport disorder. Should they or their first-degree relatives be now told of the expected risks of developing a dementia. Or should their primary care physician be informed of the results? Or should the results just remain undisclosed in the hospital records?

In this research paper some of the other questions and problems that regulation or legislation can give rise to will be presented. The answers will necessarily be evasive, and no solutions are easy to implement. But the responses can vary according to whether professional ethical codes, moratoria, referenda, or legislation are deemed appropriate.

4. Regulation For Industry

By the year 2010 ideas derived from the Human Genome Mapping Project may account for sales of $60 billion worth of products per annum; that is half the international sales of the pharmaceutical industry in 1992. New genetic knowledge translated into products will make a profit in almost any marketplace in the developed world. The profit motive is already starting to threaten the spirit of collaborative enthusiasm and cooperation in the fields of scientific research. To give just one example: there is a primitive tribe of hunter-gatherers, the Hagahai, living in a remote and inaccessible mountain range of Papua New Guinea. There was a suspicion from epidemiological studies that some of them were making anti-bodies to a virus that can cause a cancer of the blood, leukemia. Cells were taken from a young man of the tribe and cultured in the laboratories of the National Institutes of Health (NIH) in Bethesda, MD, USA. The cells were indeed found to be making antibodies and the NIH researchers were quick to see the profits to be made out of them. They applied for patent rights relating to the cell line. It was agreed that the Hagahai should receive some (unspecified) share of any commercial profits arising from the ‘invention.’ In 1996 the patent was officially disclaimed by the NIH after a heated international controversy developed about the exploitation and biocolonialism of primitive peoples (A. Pottage in Law and Human Genetics, Brownsword et al. 1998).

It can be seen that cells and genes of remote rural peoples are becoming the intellectual property of corporations and government institutions that hope to use the proceeds to fund their genetic and research laboratories. They claim in justification that free market incentives and the profit motive are the best and most efficient way to advance types of basic medical research which are very costly.

4.1 Databases

The Icelandic parliament passed a bill in December 1998 to make it legal for a private company, deCODE Genetics, to acquire a comprehensive database containing the very detailed medical records of almost the entire population of Iceland, about 270,000 persons. This database is of vital interest because it contains large family trees for the vast majority of the population, and the records have been kept meticulously up-to-date. Iceland has an isolated population with very little immigration for the best part of 1,000 years. It is therefore an ideal population to investigate for the genetic basis of disease. deCODE Genetics, largely funded by American investors, has signed a contract with the Swiss pharmaceutical giant, Hoffman La Roche, worth about $200 million giving them exclusive access to the database to search for the genetic origins of 12 common diseases. It could be considered that the entire population of Iceland is being turned into a biomedical research commodity with a large commercial potential. The DNA part of the database is now being collected and will cover about 90 percent of the Icelandic population. Opposition to the bill was based on three major arguments. (a) There would be no individual signed consent for transfer of the health information to third parties and this would constitute an unwarranted invasion of privacy. (b) It may lead to loss of trust in the confidentiality of the doctor–patient relationship even if the health information were to be encrypted before the transfer. (c) Finally a monopoly was being given to one company to pursue this research. The project will cost about $150 million— more than twice the entire research budget for Iceland. So proponents argue that a private company is needed to fund the project since no governmental agency would have the marketing experience or readiness to float such a venture. The bill was finally passed and the DNA part of the population database is being assembled (Galton and O’Donovan 2000).

Such accurate and extensive medical records combined with a matching DNA bank could provide a Cornucopia to uncover the genetic origins of many diseases and be of inestimable health benefit to Icelanders as well as other populations. But if the database were to fall into the wrong hands it could provide yet another means for discrimination against an ‘undesirable’ or minority element in society. Passing the act also broke one of the fundamental principles of scientific research: that any research plans have to be evaluated and approved by an independent ethics committee before recruitment of patients should begin. deCode managed to convince the Icelandic government to pass the laws which avoided the necessity for review by a Bioethics or data protection committee. The government claimed that the act resulted from an informed democratic decision, but only 13 percent of the nation considered themselves to have a good enough grasp of the nature of the bill according to a Gallop poll conducted in November 1998. The act was passed by the Icelandic parliament before the public really understood all the issues. A provision in the bill ensures that the database will remain anonymous and therefore informed consent is not necessary. This then raises the problem that if some Icelanders are found to possess genetic variants that predispose them to a serious and treatable disorder they will not be told about it. Yet it is the doctors duty to inform such patients, so clearly the database is not going to be as anonymous as initially promised. The more genetic technology that is introduced into society, especially by Industry, the more important it becomes to protect the rights of individuals from becoming subservient to either state procedures or becoming exposed to market-led commercial forces (Berger 1999).

5. Regulation Of Home Genetic Testing

‘Do-it-yourself’ tests for detecting pregnancies or genetic identification of paternity have been a recent commercial success. The discovery that genetic variants that predispose to some types of inherited forms of cancer has provoked widespread public interest. Demands for home tests by the public have been partly satisfied by commercial laboratories. Tests for genetic variants that cause a rare cancer of the large bowel have been put on the market and performed by a private company La Corp (Baltimore, MD, USA) after referral by a doctor. Many inadequacies and errors were found in the use of this service. In a study conducted in 1995, 177 patients were tested but only 19 percent received genetic counseling before the test to explain what was going to happen. Only 17 percent provided informed consent to have the test. In 32 percent of the cases the referring doctor misinterpreted the test results. Some patients at risk of developing the cancer were given false negative results because the tests were not done on affected family members to see which particular genetic variant occurs in that family. The scope for misapplication and misinformation of patients and creation of public anxiety in view of the other variable factors that can influence the final outcome are enormous. Yet already other commercial DNA-based tests are appearing. One developed by Oncor has received recent Food and Drugs Administration (FDA) approval in the USA to be used for risk prediction for the recurrence of breast cancer. Clearly regulation and tests of quality for the use of these measurements in the marketplace are going to be required for the future to protect the public from errors and the generation of unnecessary anxiety (Galton and Ferns 1999).

6. Life And Health Insurance: Disease Prediction

In its simplest form life or health insurance is a way of relieving the harmful effects of chance events such as disease or accidents. By pooling the modest premiums from a large number of people who are at the same risk, this can provide resources for making large payments to those who suffer harm or damage.

Standard insurance forms represent voluntary contracts between an individual and the insurance company and ask details about recent medical treatment, medical conditions, and family medical history. Insurance companies may require medical examination or consent for access to medical records. Assessment of risk plays a part in making the insurance contract and it is for the proposer to disclose the information required or otherwise withdraw from the contract. Failure to disclose is likely to lead to a void contract in case of a claim.

There are several ways such health or life insurance could be organized. There are basically three types of models: solidarity, mutuality, or altruism. Insurance based on solidarity takes no account of the different levels of risk that individuals bring to the pool; premiums are set at a uniform level, or based on the ability to pay. The British National Health Service is a good example of this type. Insurance based on mutuality relates the premiums to be paid to the level of risk each person brings to the common pool. The premiums will therefore vary with risks involved. A car driver with a clean driving record obtains a lower premium for car insurance than drivers with a careless record. This is perhaps fair because the bad driver could have taken more trouble to avoid the accidents. Conversely, penalizing someone with higher premiums through no fault of his or her own because they have inherited some faulty genes seems unfair—it is like financially punishing them for their skin color. Everyone from birth onwards has the chance of contracting one of a variety of afflictions that could be associated with defects in their DNA, but not all of these will come to light. Calculation of such risks can be difficult, and risk prediction for disease in life and health insurance may draw heavily on the genetic details of the person. Finally, insurance based on altruism argues that an individual should not be penalized for the chance inheritance of unfavorable genes over which he or she has no control, and that if anything health insurance as an instrument of social justice should be made cheaper not more expensive for them. This would be a noncommercial operation and would probably require that government provides some sort of a support system.

In the UK most life insurance is commercially organized and based on mutuality, whereas most health insurance in the UK is organized by the National Health Service, based on solidarity. For life insurance this means that the insurers try to adjust the premiums to match the risks involved. For single gene disorders such as the muscle wasting disease (Duchennes’ muscular dystrophy) or cystic fibrosis, this is not difficult to do since if the individual possesses the bad genes he/she will almost certainly go on to develop the disease. The usual underwriting practice of insurance companies is to accept people with a family history of Huntington’s disease who have not been tested but to charge them higher premiums. People known to carry the gene for Huntington’s disease are usually refused cover (although they can obtain considerably better annuity rates if they retire because their life expectancy is reduced). However, for more complex disorders such as heart attacks, diabetes, or high blood pressure, the calculated risks are far more uncertain. Genes may be involved not in causing the disease, but in conferring a predisposition or susceptibility to the disease. Prediction of risks will be uncertain because of two major factors: (a) the disease will often not become apparent unless certain environmental conditions are encountered and (b) there is a variable interaction among genes that can modify the severity of the disease. A women carrying the susceptibility genes for diabetes mellitus may not manifest the disease until she becomes pregnant. The pregnancy in some way tips her into the diabetic state and her blood sugars rise and she passes sugar in her urine. After the pregnancy the diabetes disappears, but may recur at a later date as the women ages or becomes obese. As an obese person with diabetes she may sometimes see the disease disappear if strict dieting results in weight loss. How then should her premiums be adjusted if the declared aims are to take risks into account? As a general rule the risk is calculated at the time of taking out the insurance—if not diabetic at the time then no increased premium is applied.

The insurance industry in the UK has already laid out guidelines for the disclosure of genetic tests before the purchase of life insurance, disability income insurance, and critical illness cover. The Association of British Insurer’s code of practice (UK) recommends that for purchase of life insurance up to a total of £100,000 which is directly linked to a new mortgage for a private dwelling, the results of any genetic tests must be reported but may not be taken into account by the insurance company. It is implied that for sums greater than £100,000 such genetic tests will be taken into account and the premiums adjusted accordingly. Companies insist that premiums paid must truly reflect the extent of risks of disability. Otherwise people at high risk will purchase higher claim policies and stand to make a financial gain out of the premiums paid by the lower risk individuals. This would be robbing the common pool of people of their money paid as premiums. The insurance industry is a commercial organization and cannot subsidize one type of policyholder who may withhold information on his her genetic risks by charging the rest of the policyholders more than the appropriate premiums. The insurance industry calls this ‘adverse selection’ or ‘ antiselection’ and although their arguments are rather bureaucratic in tone they are socially very important. There is already evidence that antiselection operates on the purchase of insurance products at rates above £100,000. However, if after genetic testing you cannot obtain a mortgage, this may discourage one from starting a family. This can result in an indirect eugenic effect.

Insurance companies in the UK cannot make applicants take genetic tests but if a test has already been taken the result must be given to the insurer if it asks for that information. If a genetic test is taken after the policy has been bought the insurer cannot ask for the results. For example, a woman aged 30 years with a known mutation in the breast cancer gene (BRCA1) may have a seven-year reduction in life expectation. If she has had the genetic test the insurers would expect her to pay a higher premium. The new genetic tests for chronic illness such as diabetes, dementias, or Parkinson’s disease may profoundly affect the purchase of long term care insurance or critical illness cover by individuals and leave many people unprotected when they come to need most help. In the future the state will probably have to intervene to provide some form of protection for such people.

Insurance companies often decline to insure against pre-existing conditions. Does the possession of a liability gene for, say, Alzheimer’s dementia constitute a pre-existing condition? Do such people, although healthy now, come into the category having a disease? If having a genetic defect counts as a disease, then the whole population would come into a disease category. We all possess some deleterious genetic variants, but they may never come to light as disease unless we encounter a particular set of environmental conditions. However, risk discrimination by insurers could be the slippery slope leading to a social underclass on the basis of their genetics who will find it impossible to afford any form of health or life insurance (Law et al. 1998).

To deal with this problem of ‘adverse selection,’ the European Council at Strasbourg in their document on Human Rights and Biomedicine (1997) stated that ‘any form of discrimination against a person on the grounds of his or her genetic heritage is prohibited.’ But there is already some evidence that insurance companies are dealing unfairly with relatives of families where a genetic disease occurs. The data come from a postal survey of 7,000 members of seven different British support groups for families with genetic disorders such as cystic fibrosis, Huntingdon’s disease, and muscular dystrophy; and a sample of 1,033 members of the general public (Law et al. 1998). The response rate to the postal questionnaire was rather low as is usual with the number of questionnaires that are currently being circulated. About 13 percent of respondents who represented no actuarial risk on genetic grounds, either being healthy carriers or being altogether unaffected, had perceptions that they had been discriminated against on the basis of their family history. They were asked to pay higher premiums or were refused insurance outright. This may have been simply due to confusion or ignorance about genetic disease on the part of the medical officers employed by the insurance company; or possibly a way for them to try to avoid adverse selection of people who they thought were at increased risk of an inherited disease. Or it may be the respondents thought they were being victimized by their family history when in fact this was not the case. Clearly the claims for actuarial fairness by the insurance industry and the claims for social justice by the European Council will require new forms of regulation to clarify this problem. One possible solution might be to set up a type of state insurance scheme rather like the National Health Service so as to avoid penalizing individuals who have been given a bad genetic constitution through no fault of their own. In this case compensation would be paid by the more fortunate members of the rest of society who through no merit of their own inherited a good set of genes. Private insurance would still have a place alongside the State Insurance Scheme in the same way that Private Medicine operates alongside the NHS. But to many people it appears fair for the state to redistribute resources from the genetically lucky to the genetically ‘underendowed.’

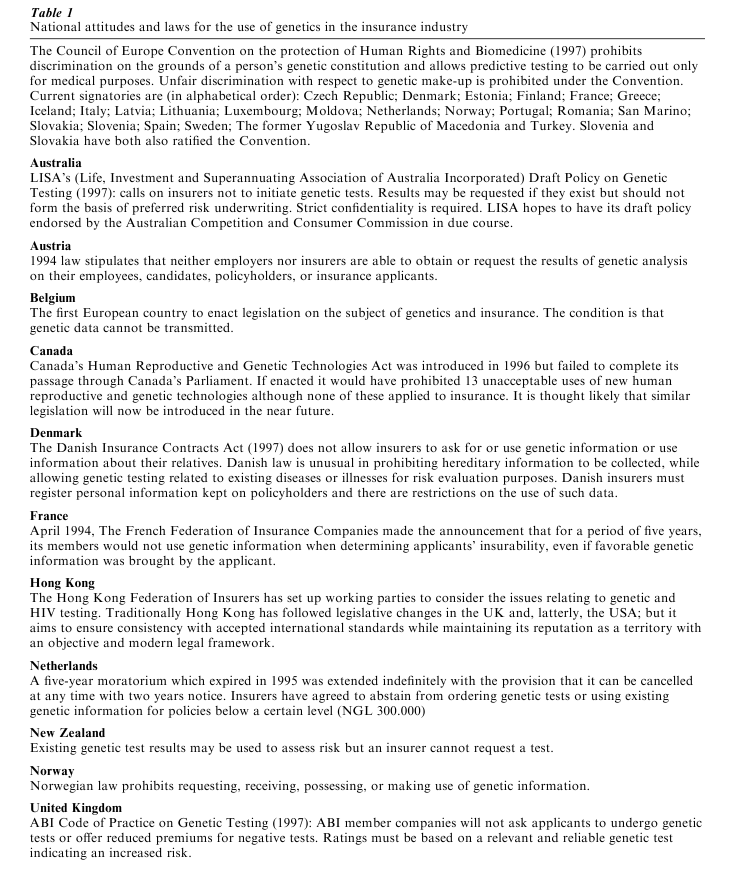

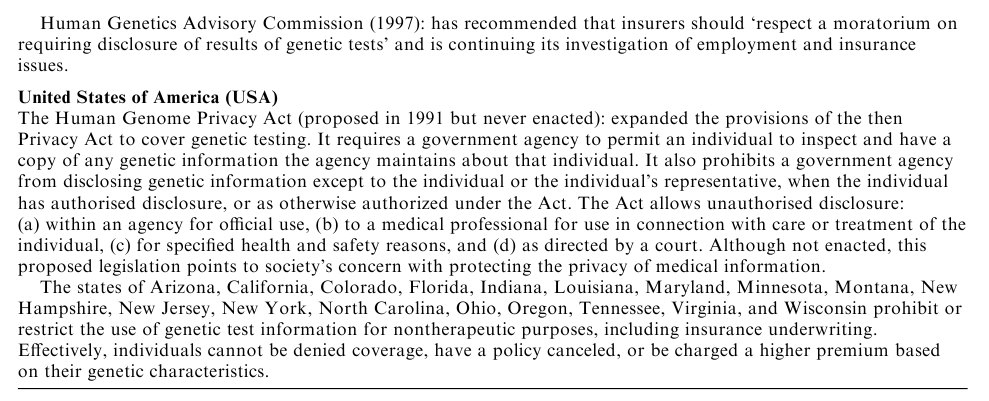

The responses of other European countries to the problem of adverse selection and genetic discrimination are presented in Table 1.

In the USA where health insurance is commercially organized and based on a mutuality model, many people have no health insurance at all. A great deal of recent legislation has aimed to restrict the use by health insurers of genetic tests and more broadly of any ‘genetic information.’ Federal legislation enacted in 1996 forbids insurance companies from using even family history to exclude people from schemes for group health insurance. The state of New Jersey has gone further and bans the use of genetic information for any insurance or employment purposes without written consent of the person involved. They have not suggested any practical measures to prevent adverse selection but appear to be making it easier for some groups to obtain health insurance. This is to prevent the trend for health care in the USA being converted from a social service to an economic commodity, sold in the marketplace and distributed on the basis of who can afford to pay for it (Pokorski 1997).

Bibliography:

- Appleyard B 2000 Brave New Worlds. Harper Collins, London

- Association of British Insurers 1997 Life Insurance and Genetics. A policy statement of the Association of British Insurers

- Berger A 1999 Private company wins rights to Icelandic gene database. British Medical Journal 318: 11

- Brownsword R, Cornish W R, Llewlyn M (eds.) 1998 Law and Human Genetics. Hart Publishing, Oxford, UK

- Duster T 1990 Backdoor to Eugenics. Routledge, New York

- European Commission of Advisors on the Ethical Implications of Biotechnology 1996 The Ethical Aspects of Prenatal Diagnosis. European Commission of Advisors on the Ethical Implications of Biotechnology, Brussels

- Galton D J 2001 In Our Own Image: Eugenics and the Genetic Modification of People. Little Brown & Co., Boston

- Galton D J, Ferns G A A 1999 Genetic markers to predict polygenic disease: A new problem for social genetics. Quarterly Journal of Medicine 92: 223–32

- Galton D J, Galton C J 1998 Francis Galton: And eugenics today. Journal of Medical Ethics 24: 99–105

- Galton D J, O’Donovan K 2000 Legislating for the new predictive genetics. Human Reproduction and Genetic Ethics 6: 39–47

- Galton D J, Krone W 1991 Hyperlipidaemia in Practice. Gower Medical, London

- Great Britain. Parliament. House of Commons, Science and Technology Committee 1995 Human Genetics: The Science and its Consequences. HMSO, London

- Harris J 1998 Clones, Genes and Immortality. Oxford University Press, Oxford, UK

- Kennedy I, Grubb A 1994 Medical Law. Butterworths, London, pp. 666–9

- Kevles D J 1995 In the Name of Eugenics. Harvard University Press, Cambridge, MA

- Kevles K J, Hood L (eds.) 1992 Scientific and Social Issues in the Human Genome Project. Harvard University Press, Cambridge, MA

- Kitcher P 1996 The Lives to Come. Penguin, Harmondsworth, UK

- Law L, King S, Wilkie T 1998 Genetic discrimination in life insurance: Empirical evidence from a cross sectional survey of genetic support groups in the UK. British Medical Journal 317: 1632–5

- Lewontin R C 1993 The Doctrine of DNA. Penguin, Harmondsworth, UK

- Peters T 1997 Playing God. Routledge, New York

- Pokorski R J 1997 Insurance underwriting in the genetic era. American Journal of Human Genetics 60: 205–16

- Powledge T 1974 Genetic screening as a political and social development. In: Bergsma D (ed.) Ethical, Social and Legal Dimensions of Screening for Human Genetic Disease. Stratton International Medical Books, New York

- Rifkin J 1999 Biotech Century. Putnam, New York

- Rose S, Lewontin R C, Kamin L J 1990 Not in Our Genes. Penguin, Harmondsworth, UK

- Weir R F, Lawrence S C, Fales E (eds.) 1994 Genes & Human Self-knowledge. University of Iowa Press, Ames, IA

- Wilson E O 1978 On Human Nature. Penguin, Harmondsworth, UK

ORDER HIGH QUALITY CUSTOM PAPER

Always on-time

Plagiarism-Free

100% Confidentiality